We have all heard the financial cliché: “Stop buying expensive coffee and you’ll become a millionaire.” In the early 2000s, this was popularized as the “Latte Factor.” But as we navigate the economic landscape of 2026, the math has evolved. Inflation, the rise of “micro-transactions,” and the digital subscription trap have turned small daily habits into massive long-term financial leaks.

If you want to truly master your money in this decade, you don’t just need a basic budget; you need to understand the Mathematical ROI of Self-Denial.

The Micro-Leak Theory: Why $5 Matters More Than You Think

“The Human Logic: Why we ignore the small bills but stress over the big ones.”

Most people spend hours sometimes days researching a $500 smartphone purchase. Yet, they won’t spend five seconds thinking about a $7 daily energy drink, a $5 delivery tip, or a $15 monthly streaming service they haven’t opened in weeks. This is a cognitive bias known as Denomination Effect. We categorize small purchases as “disposable,” while large ones are “investments.”

However, in the world of high-stakes finance, consistency beats intensity. A $5 daily habit isn’t just a $5 loss; it is the opportunity cost of what that money could have earned if it were working for you. In 2026, where micro-investing apps allow you to buy fractional shares with a single click, every dollar has the potential to be a “seed” for a future money tree.

The 2026 Math: The Deadly Duo of Inflation and Compounding

“Dissecting the Trap: Why ‘Cheap’ habits are getting exponentially more expensive.”

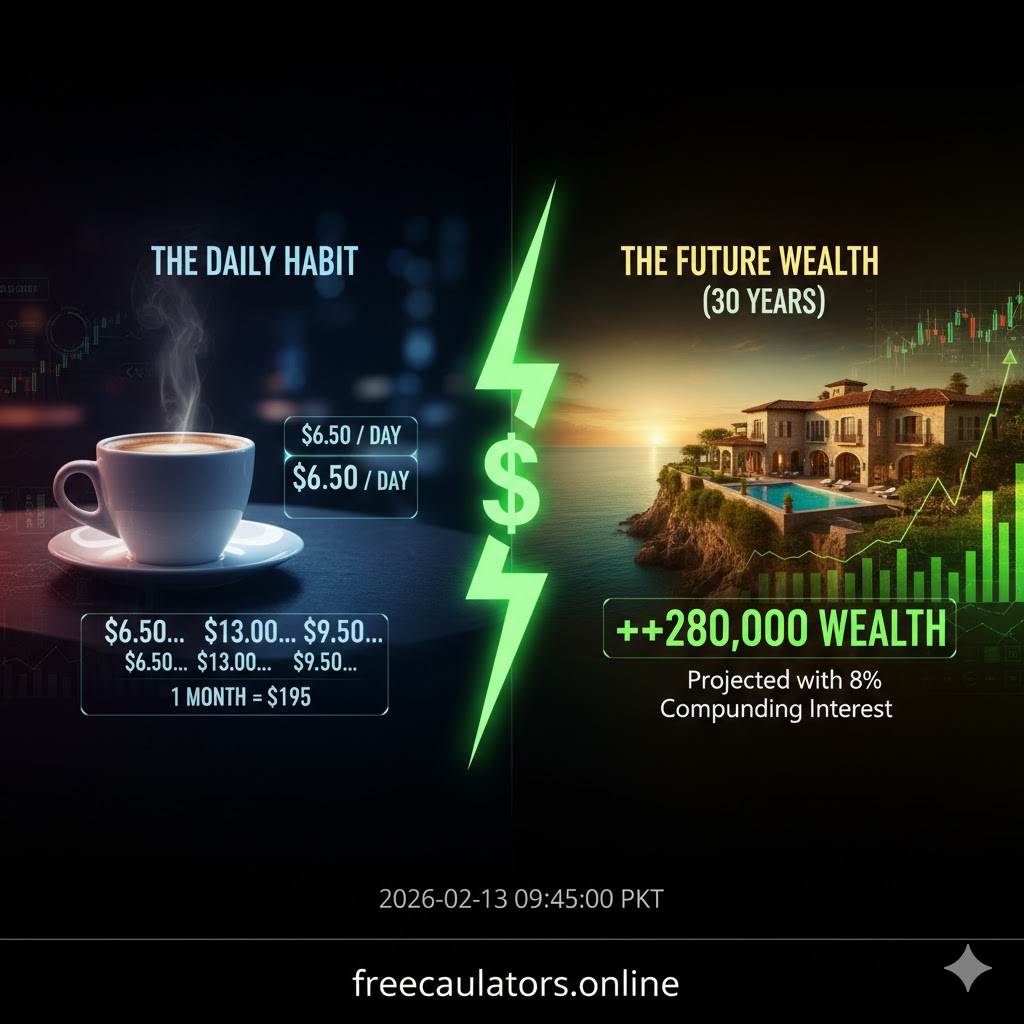

In 2026, the “Latte” that cost you $3.50 back in 2015 now costs $6.50 due to the rising costs of dairy, transport, and labor. When you look at this through the lens of Compound Interest, the numbers are staggering.

If you take that $6.50 and invest it daily into a diversified portfolio with an average 8% annual return:

- In 10 Years: You would have approximately $35,000.

- In 20 Years: You would have over $110,000.

- In 30 Years: That daily coffee has cost you nearly $280,000.

But it’s not just coffee anymore. The “Modern Latte Factor” has expanded into our digital lives:

- Ghost Subscriptions: The “Free Trial” you forgot to cancel in 2025.

- Convenience Premium: Paying 40% extra for food delivery just to save a 10-minute walk.

- In-App Purchases: Small $1.99 gaming “power-ups” that bypass our brain’s financial defense system.

The Recovery Formula: Turning Small Savings into Large Assets

“The Wealth-Builder Math: How to calculate the ‘Future Value’ of your cravings.”

The goal here isn’t to live a life of total deprivation. A life without joy isn’t a life worth living. The goal is Value-Based Spending. If that morning coffee is the only thing that gets you through a tough 9-to-5, then it has high utility. But if it’s just a mindless habit you do out of boredom, it’s a leak.

Use this simple logic to test every recurring expense:

$$Total Impact = (Daily Cost \times 365) \times (\text{Years of Habit})$$

By using a Compound Interest Calculator, you can visualize the “Future Debt” you are creating for your future self. When you see that a daily habit is actually a $200,000 decision, your perspective on “it’s only five dollars” changes instantly.

The 2026 Strategy: The “Automated Sacrifice” Method

“How to secret-proof your future by gamifying your bank account.”

The smartest way to beat the “Latte Factor” today is to automate your discipline so you don’t have to rely on willpower.

- The “Switch & Save” Hack: If you decide to make coffee at home instead of buying it out, immediately open your banking app and transfer that $6 into a high-yield savings account or a crypto-index.

- The Subscription Audit: Every 3 months, use a Finance Tracker to list every recurring bill. If you haven’t used the service in 30 days, kill it immediately.

- The 48-Hour Rule: For any non-essential purchase under $20, wait 48 hours. If you still want it, buy it. Usually, the “impulse” dies before the timer ends.

Watching an investment account grow from $0 to $10,000 purely from “saved coffee money” is far more rewarding than any caffeine hit. It’s about moving from being a Consumer (who pays for others’ dreams) to an Owner (who builds their own).

Conclusion: Small Hinges Swing Big Doors

“Your financial freedom isn’t found in a ‘big break’; it’s found in small choices.”

Don’t let the simplicity of the “Latte Factor” fool you. It is the most powerful concept in personal finance because it is actionable today. You don’t need a promotion or a lottery win to start building wealth; you just need to stop the leaks.

Before you make your next “small” purchase, ask yourself: “Is this worth a villa in 2050?” The math says it might be.